Reimagining Personal Finance through Behavioral Habits

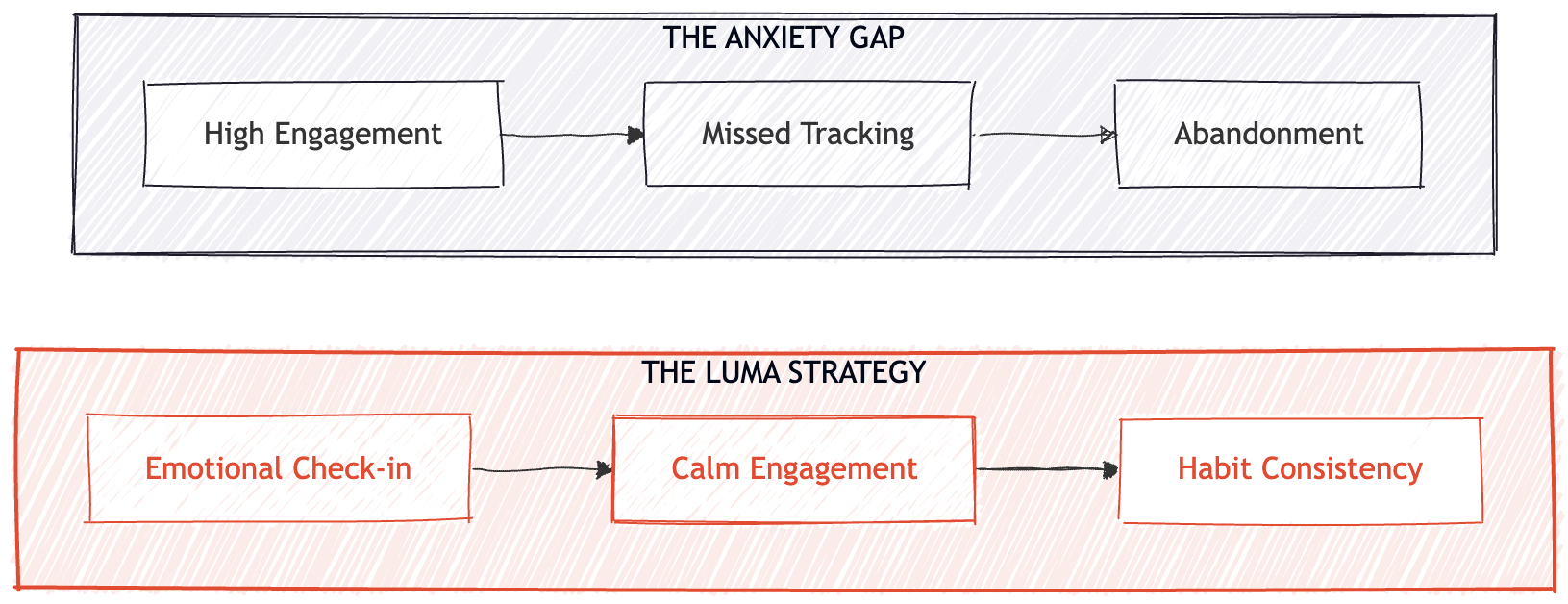

Strategic Objective / The Anxiety-Accounting Gap

Most finance apps treat money as a math problem. Track every transaction, categorise every purchase, surface a dashboard full of numbers. The logic is sound but the assumption is wrong. Users with money anxiety don't fail because they lack data. They fail because the apps make them feel judged.

Luma starts from a different premise entirely: money problems are behavioral, not mathematical. Fix the emotional relationship with money first, and the financial outcomes follow.

The strategic objective was to build a habit-first financial coach that prioritises emotional awareness and consistency over perfect ledger reconciliation. Not track every cent but build a healthier relationship with money over time.

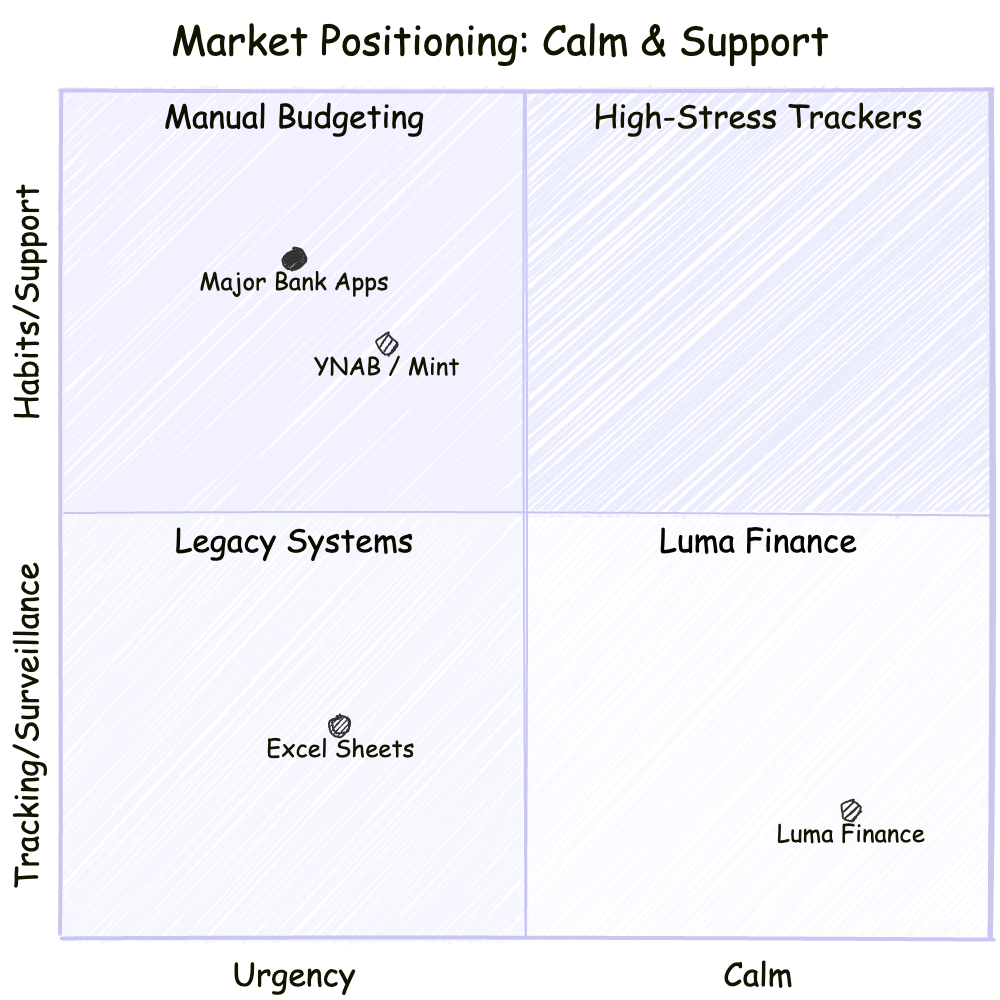

Product Positioning / From Surveillance to Support

The personal finance app market is saturated — but saturated in one direction. Every major player frames money management as a performance metric. Green means winning, red means failing. The entire category is built around urgency and accountability.

That created a clear white space: a product that leads with support, not surveillance.

The target persona is the Independent Earner — ages 25-40, has tried budgeting apps and quit, earns enough but feels anxious about money. Optimised for Reflection over Reaction and Consistency over Perfection.

Core Product Loop / Check-in → Reflect → Adjust

The central design challenge: how do you keep users engaged with their finances without triggering a stress response? The answer was to change the entry point entirely.

Unlike every other app, the entry point isn't a transaction list. It's an emotional check-in: "How did today feel financially?" This reframes the relationship from auditor to coach. The loop is designed to take under 2 minutes and feel like journaling, not accounting.

The product is also explicitly designed for imperfection. Missing a day resets gently, not punitively. Partial tracking is supported by default. The all-or-nothing barrier that kills engagement in traditional apps is removed by design.

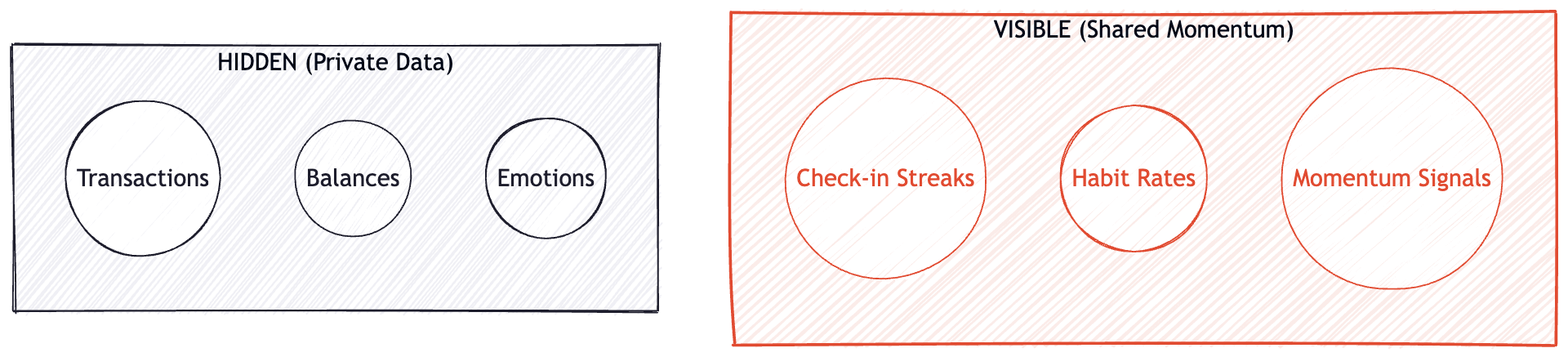

Identity & Privacy / Shared Intent, Not Shared Control

Shared finances are a minefield. Couples or accountability partners sharing financial data often creates pressure and judgment — the opposite of what Luma stands for. The challenge was to solve for social motivation without creating surveillance.

The privacy logic is designed so that even a curious or controlling partner cannot extract meaningful financial data. What they see is aggregate signal — momentum, not money.

MVP & Outcomes / Defined as Much by What Was Cut

The hardest PM skill is knowing what not to build. Luma's V1 is as much a story of restraint as it is of design.

The temptation with a finance app is to integrate with banks immediately — it feels like the "real" version of the product. But bank integrations in V1 would have shifted focus from habit-building to transaction-tracking. That's exactly the pattern Luma is trying to break. They're deferred to V2 deliberately — a product philosophy decision, not a resource constraint.